If you’re researching mortgages, you know that they come with interest rates. What exactly is a mortgage interest rate, and how much does it impact your buying power? What can you do to improve the interest rate you’re offered? We answer those questions in this article.

Your mortgage interest rate has a direct impact on how much house you can afford. What exactly is a mortgage interest rate?

A mortgage is a loan, and like other bank loans, it comes with an interest rate – it’s how lenders make enough money to stay in business. This is usually a percentage of the loan amount, and you pay it off alongside the principal. Usually, this makes up your monthly mortgage payment, along with things like private mortgage insurance (PMI), property taxes, and perhaps homeowner insurance.

How Your Mortgage Interest Rate Affects You

As the interest rate is part of your monthly mortgage payment, it directly affects how much of a loan you can afford. Even a small change in your interest rate can add quite a bit. For example, let’s say you bought one of Michigan’s average-priced houses for $210,000.

You managed a 10% down payment and got a conventional 30-year loan. At a 4% interest rate, you’re paying 1,264.40 per month. At 5% interest, this payment increases to $1,376.68. That’s $112 more per month – and 10 more PMI payments.

So, it’s pretty obvious how much your budget is impacted by mortgage interest rates. But what factors affect the interest rates themselves?

What Affects Mortgage Interest Rates?

Banks calculate interest rates based on many things, including the overall economic and market picture and the qualifications of each prospective borrower. We’ve already talked about factors that influence mortgage interest rates elsewhere in this blog, so let’s just do a quick overview of some of the factors you can influence:

Your credit score and credit history.

Your income and debt.

Your down payment amount.

The type of loan you choose.

Although a lot has been said about the Federal Reserve rate rising, it’s important to realize that this doesn’t directly affect your mortgage interest rate. (It does affect other types of loans, like credit cards.) However, the Fed is a good indicator of where the economy is heading, so it doesn’t hurt to keep an eye on it.

https://www.michmortgage.com/wp-content/uploads/2022/10/fall-stoop.jpg900900Courtney Coonhttp://www.michmortgage.com/wp-content/uploads/2017/12/MM-for-white-background-300x105.pngCourtney Coon2022-10-13 11:56:132022-10-13 11:56:13How do interest rates impact your home buying power?

With the interest rates increasing, it’s important to find ways for buyers to continue to buy properties and have payments they can afford. A “Buydown” is a great way to do that.

Buydowns come in the form of 3-2-1, 2-1 and one-year buydowns.

How it works: funds from the seller pre-pay the buyer’s payment for 1, 2 or 3 years. For example, on a 2-1 Buydown, the interest rate is 2% lower than market in the first year, 1% lower the second year and market the third year.

Let’s assume a home is being sold for $300,000 and the buyer is putting 5% down. To attract more buyers, the seller has agreed to pay $6,100 toward a 2-1 Buydown. If the current market rate is 5.5% then the buyer’s payment for the first 12 months would be at 3.5% or $1,279/month. For the second year, the payment would be based on a rate of 4.5% or $1,444/month. Starting in the third year, the buyer’s payment would be at 5.5% for the remaining 28 years or $1,618/month.

The cost is calculated by taking the difference between payments in year one and your 3×12 plus the difference between payments in the year two and year 3×12. In our example above the total cost would be $6,100. The monthly reduction in payment for the first year would be $339 and the $174 during the entire second year.

This may be a much more attractive option for a buyer than going into some sort of an adjustable rate (ARM) product that has more risk with it. Remember, an ARM will eventually adjust to the market rate and there is no guarantee that rates will be lower when that ARM starts to adjust.

The Buydown uses current market rates but allows the buyer to buy a home at a more affordable price with the risk of the ARM. Additionally, this a great way for buyers who are likely to make more money as they continue their career to ease into the payment.

But what is in this for the seller. Why would they do this? The answer is that the seller May be willing to concede $6,000 more readily than dropping their sale price by $10,000 or $15,000 when their house is not selling. Additionally, by offering this option to buyers they may get more interest from more buyers creating more competition.

We used to do 2-1 Buydowns years ago when rates were higher. But for the last several years with rates at all-time lows, they were forgotten. Now that rates are creeping up again, it may be good time to blow the dust off this product and help more buyers realize their dreams.

If you have questions about 2-1 Buydowns, give us a call! We’re happy to help in any way we can.

https://www.michmortgage.com/wp-content/uploads/2022/08/Welcome-on-door.jpg900900Rob Garrisonhttp://www.michmortgage.com/wp-content/uploads/2017/12/MM-for-white-background-300x105.pngRob Garrison2022-08-03 10:31:532022-08-03 10:38:29Beat the Rates with a Buydown Program

For first-time buyers, the mortgage process raises a lot of questions. In part two of this series, we tackle some more of the most common questions we receive from customers.

“How Much Should I Save for a Down Payment?“

The exact dollar amount you should save for a down payment depends on the price of the house you are buying. Most down payment requirements are expressed in percentages. A 5% down payment on a $500,000 house is much greater in raw dollars ($25,000) than 5% on a $200,000 house ($10,000).

In terms of the minimum requirements for different loan types:

For USDA or VA loans, no down payment is required.

For FHA loans, the minimum down payment is 3.5%.

For FannieMae HomeReady loans, the down payment is 3%.

On a conventional loan, the minimum down payment will be somewhere between 3% and 5% of the purchase price. Be aware, however, that you will have to pay private mortgage insurance (PMI) if your down payment is less than 20% of the purchase price.

“What Will My Monthly Payment Look Like?“

A mortgage payment consists of two components:

Principal

Interest

The principal portion goes toward paying off the original amount of money you borrowed. The interest portion covers the cost of borrowing.

Your mortgage payment will be the same amount each month. Early in the life of the loan, more money goes toward interest than principal. Over time, the principal portion will match and then exceed the interest amount. For example, on a 30-year $200,000 mortgage at 4%, your monthly payment is $955. For the first payment, $288 goes toward principal and $667 goes toward interest. It isn’t until the 153rd payment that the interest and principal are roughly equal. Thereafter, more of the monthly payment goes toward principal until, on the very last payment of the schedule, $952 goes to principal and $3 to interest.

Your lender will provide you with an amortization schedule that shows a month-by-month P&I (principal and interest) breakdown for your loan.

For convenience, many people include property tax and insurance payments in their monthly mortgage payment. Technically, these aren’t part of the loan, but the loan servicer can put this money into an escrow account, where it is saved until the taxes and insurance are due. They then make the payments for you. You are not required to include escrow in your monthly payments. If you choose not to, you will just pay your property taxes and insurance annually on your own.

“Which Loans Are Best for First-Time Buyers?“

Along with conventional loans, the following loans offer distinct advantages for first-time buyers.

FHA loans. A Federal Housing Administration (FHA) loan is a mortgage that is insured by the Federal Housing Administration (FHA) and issued by an FHA-approved lender such as Mortgage 1. FHA loans are designed for low-to-moderate-income borrowers; they require a lower minimum down payment and lower credit scores than many conventional loans.

VA loans. VA loans are offered through the Department of Veterans Affairs. They are available to active and veteran service personnel and their families. VA loans are backed by the federal government and issued through private lenders like Mortgage 1. VA loans have favorable terms, such as no down payment, no mortgage insurance, no-prepayment penalties, and limited closing costs.

USDA loans. Rural Development home loans are low-interest, fixed-rate loans provided by the United States Department of Agriculture. The loans do not require a down payment. The loans are financed by the USDA and obtained through private lenders, such as Mortgage 1, and are meant to promote and support home ownership in underserved areas.

MSHDA loans. The Michigan State Housing Development Authority (MSHDA) offers down payment assistance to people with no monthly payments. The down payment program offers assistance up to $7,500 (or 4% of the purchase price, whichever is less).

“Can I Complete the Mortgage Process Online?“

Yes! Every Michigan Mortgage loan officer has a Home Snap digital application that allows you to complete the application process online. You can get approved in as little as 15 minutes. The app lets you submit your information, communicate with your loan officer, and track the status of your loan. In these times of COVID and social distancing, Home Snap is the perfect solution.

“What is PMI?“

Private Mortgage Insurance (PMI) is an insurance policy that protects a mortgage lender or title holder if a borrower defaults on payments, passes away, or is otherwise unable to meet the contractual obligations of the mortgage. If you pay 20% or more as a down payment on a conventional loan, you do not need PMI. Once you start paying PMI, it goes away in two ways: (1) once your mortgage balance reaches 78% of the original purchase price; (2) at the halfway point of your amortization schedule. For example, if you have a 30-year loan, the midpoint would be 15 years. At the point, the lender must cancel the PMI then, even if your mortgage balance hasn’t yet reached 78% of the home’s original value. PMI is typically between 0.5% to 1% of the entire loan amount.

“What Do I Need to Bring to Closing?“

Closing is when you sign the many documents that finalize your purchase. The closing is usually held at a title company’s office. The seller will be there, as will your agent. In terms of what you should bring:

Photo ID: The closing agent has to verify that you are who you say you are. A driver’s license or current passport will do.

Cashier’s or certified check: This is to cover any down payment and closing costs you owe. Do not bring personal check or cash. Your lender will tell you how much the check should be and who it should be made out to.

Proof of insurance: The closing agent needs to see proof that you have the insurance in effect on closing day and a receipt showing you’ve paid the policy for a year. They may have already collected that, but it doesn’t hurt to bring your own copy just to ensure things go smoothly.

Final purchase and sales contract: Just in case you need to double-check anything against the actual closing costs.

“What Happens If My Appraisal is Low?“

When determining the size of your loan, lenders use a formula called loan-to-value (LTV). When your mortgage contract is initially written, LTV is calculated using the purchase price. But the final contract is based upon the official appraised value of the house. What happens if the appraised value comes in lower? You have several options.

Boost the amount of your down payment. This will allow you to meet the LTV and down payment minimums.

The seller can lower the price. The seller can agree to drop the sales price of the house to match the appraised value. This will allow you to meet LTV.

Dispute the appraisal and ask for a new one. If you think the appraiser undervalued the house, you can ask for a new appraisal.

Cancel the purchase. If a compromise can’t be reached, you can cancel the home purchase agreement.

“What Will Mortgage Rates Be Next Year?“

Ah, if only we had a crystal ball. We can’t predict what mortgage rates will be in a year, but we can say that rates today are near historic lows. The Federal Reserve announced recently that they will be holding short-term interest rates steady for the foreseeable future. While mortgage rates aren’t tied specifically to short-term interest rates, the two generally track closely together. So, while we can’t predict what rates will be in a year, we can say with certainty that today’s rates are at historic lows.

Got Questions? We’ve Got Answers

If you have questions, let us know. At Michigan Mortgage, we specialize in helping first-time buyers understand the mortgage process.

This blog post was written by experts at Mortgage 1 and originally appeared on www.mortgageone.com. Michigan Mortgage is a DBA of Mortgage 1.

https://www.michmortgage.com/wp-content/uploads/2020/10/Meeting2.jpg620620mimortgagehttp://www.michmortgage.com/wp-content/uploads/2017/12/MM-for-white-background-300x105.pngmimortgage2020-10-22 11:24:472020-10-22 11:25:18First-Time Buyer FAQ — Part 2

For first-time buyers, the mortgage process raises a lot of questions. In this article, we tackle some of the most common questions we receive from customers.

“How Does a Mortgage Work?”

Technically speaking, “A mortgage is a debt instrument secured by the collateral of specified real estate property, that the borrower is obliged to pay back with a predetermined set of payments.” (Investopedia.com)

What does that mean in plain English? It means, when you get a mortgage, you are (1) borrowing money from a lender and (2) committing yourself to paying back the money you borrowed in equal monthly payments for the length of the loan.

Because a house can be expensive, mortgage payments are usually spread over 15 or 30 years, making the cost affordable.

Your mortgage payment will consist of principal and interest portions. The principal portion goes toward reducing the amount of money you originally borrowed. The interest portion goes toward paying off the interest, which you can think of as the fee the lender charges to loan you money.

You can make additional payments, if you want, but at the least you need to make your minimum monthly payment each month.

“What Types of Loans Are There?”

Mortgage lenders offer a wide variety of loans designed to meet the needs of buyers. The most common types of loans obtained by first-time buyers are:

Conventional loans. This is the most common type of mortgage loan. Conventional loans can be for as long as 30 years or as short as five years, with options in between. They can be fixed-rate or adjustable rate. Conventional loans are provided by banks as well as private mortgage lenders like Mortgage 1. When most people think about home loans, the conventional loan is the one they are thinking of.

FHA loans. A Federal Housing Administration (FHA) loan is a mortgage that is insured by the Federal Housing Administration (FHA) and issued by an FHA-approved lender such as Mortgage 1. FHA loans are designed for low-to-moderate-income borrowers; they require a lower minimum down payment and lower credit scores than many conventional loans.

VA loans. VA loans are offered through the Department of Veterans Affairs. They are available to active and veteran service personnel and their families. VA loans are backed by the federal government and issued through private lenders like Mortgage 1. VA loans have favorable terms, such as no down payment, no mortgage insurance, no prepayment penalties and limited closing costs.

USDA loans. Rural Development home loans are low-interest, fixed-rate loans provided by the United State Department of Agriculture. The loans do not require a down payment. The loans are financed by the USDA and obtained through private lenders, such as Mortgage 1, and are meant to promote and support home ownership in underserved areas.

MSHDA loans. The Michigan State Housing Development Authority (MSHDA) offers down payment assistance to people with no monthly payments. The down payment program offers assistance up to $7,500 (or 4% of the purchase price, whichever is less).

“How Do I Qualify for a Mortgage?”

Different mortgage types have different specific qualification requirements, but the general process of qualifying for a mortgage is the same.

You submit an application with a lender.

You provide the necessary documentation, which includes paycheck stubs, tax statements, bank and asset statements, and identification.

The lender reviews your information. They look at your income, how much debt you have, and they also pull a credit report.

Based upon your status, the lender determines how much money you can afford for a mortgage as well as what interest rate you should receive.

“What Is the Required Minimum Credit Score?”

An important element of qualifying for a mortgage is your credit score. Your lender pulls a credit report to look at your credit score. Different loan types have different qualifying scores:

The minimum qualification score for most conventional loans is 620.

For FHA loans, the minimum score is 580.

For VA loans, the minimum score is 620.

For USDA loans, the minimum score is 640.

In addition to credit score, a lender looks at your debt-to-income ratio to make sure you are not overextended.

“How Much House Can I Afford?”

To determine how much house you can afford, follow the 28/36 rule.

Many financial advisers agree that households should spend no more than 28 percent of their gross combined monthly income on housing expenses and no more than 36 percent on total debt. Total debt includes housing as well as things like student loans, car expenses, and credit card payments.

The 28/36 percent rule is the tried-and-true home affordability rule that establishes a baseline for what you can afford to pay each month.

To calculate how much 28 percent of your income is:

Multiply 28 by your monthly income. If your monthly income is $7,000, then multiply that by 28. 7,000 x 28 = 196,000.

Divide that total by 100. For example, 196,000 ÷ 100 = 1,960.

Do the same for the 36 percent rule, using 36 in place of 28 in the example above.

Got Questions? We’ve Got Answers

Come back next week for part two of this article. In the meantime, if you have questions, let us know. At Michigan Mortgage, we specialize in helping first-time buyers understand the mortgage process.

This blog post was written by experts at Mortgage 1 and originally appeared on www.mortgageone.com. Michigan Mortgage is a DBA of Mortgage 1.

For much of American history, home ownership was out of reach for most families. Prior to the 1930’s, mortgages were limited to 50 percent of a property’s market value and the repayment schedule was spread over three to five years, with a balloon payment at the end.

With terms like that, it is no wonder only four in 10 Americans at the time owned homes.

In 1934, the modern mortgage was created by the FHA. Loans from the FHA spread payments across 30 years. In doing so, they made the cost of borrowing lower and home ownership more attainable.

Today, mortgages come in a variety of lengths and terms and, in fact, are the most common type of personal loan held by households.

One thing all mortgages have in common is they charge interest. Understanding what mortgage interest is, how it is calculated, and how it impacts your payments is critical to ensuring you get the best terms possible when you shop for a mortgage.

Calculating Interest

Interest is what makes all forms of borrowing possible. Interest is the fee a lender charges for loaning money.

While a person might be willing to lend a family member money without charging interest, in the real world, nobody loans money, especially large amounts, without getting something in return to cover the risk. Interest protects and rewards the lender.

Mortgage interest rates can vary depending on market conditions and the borrower’s credit score. Today, mortgage rates are at historic lows, making home ownership more affordable than ever.

When repaying a loan, interest is the additional payment made on top of the principal. Principal is the original amount you borrowed.

The interest rate is expressed as an annual percentage rate. Calculating interest and the total amount owed is pretty straightforward.

For example, let’s say you borrow $5,000 at a simple interest rate of 3% for five years. You would pay a total of $750 in interest. The formula for calculating amount owed and interest is: P(1 + (R x T)) = A

P is the principal amount. This is how much you originally borrowed.

R is the rate of interest per year, written in decimal format (e.g., 0.03)

T is the total time in years you’ll use to pay off the loan.

A is how much you pay over the total life of the loan, including interest.

In this example, the total cost is calculated as follows: $5,000(1+(.03 x 5)) = $5,750. The difference between this number and the original loan amount is the amount of interest ($750).

Types of Mortgage Interest

There are two primary types of interest that are assigned to mortgages: fixed interest and variable interest.

Fixed Interest

The monthly payment remains the same for the life of this loan. The interest rate is locked in and does not change. Loans have a repayment life span of 30 years; shorter lengths of 10, 15 or 20 years are also commonly available.

Variable Interest

With a variable interest loan, often called ARM (“adjustable rate mortgage”), the interest rate is not locked in and monthly payment for this type of loan will change over the life of the loan. Most ARMs have a limit or cap on how much the interest rate may fluctuate, as well as how often it can be changed. When the rate goes up or down, the lender recalculates your monthly payment so that you’ll make equal payments until the next rate adjustment occurs.

What is APR?

APR stands for “annual percentage rate.” It’s a true, all-encompassing measurement of the cost of borrowing money. The APR could include fees associated with the loan. That makes the APR slightly higher than the actual base interest rate of the loan.

To calculate APR:

Add the fees and the interest paid over the entire life of the loan

Divide that by the loan amount

Divide that by the number of days you’ll be paying back the loan

Multiply that by 365

Multiply again by 100

Consider this example: You borrow $5,000 at 3% over 5 years and there’s a $150 administration fee for the loan. The APR is calculated as follows.

$150 + $750 = $900

900/5000 = 0.18

(0.18/1825) x 365 = 0.042

.042 x 100 = 4.2

The APR for this loan is 4.2%.

The Amortization Schedule

Mortgage payments are made on a monthly basis. Each month, you pay back a portion of the principal plus the interest accrued for the month. Your monthly payment remains the same for the life of the loan.

The lender will provide you with an Amortization Schedule that lists how much principal and how much interest you are paying each month. Early in the life of the loan, you will pay more interest than principal. Over time, the amount of principal paid each month increases.

For example, a $100,000 loan with a 6 percent interest rate carries a monthly mortgage payment of $599.55. For the first payment, $500 each goes toward the interest; $99.55 goes toward principal. Each month, slightly more goes toward principal; see the table below. Not until year 18 does the principal payment exceed the interest.

Payment

Principal

Interest

Principal Balance

1

$99.55

$500.00

$99,900.45

12

$105.16

$494.39

$98,772.00

180

$243.09

$356.46

$71,048.96

360

$597.00

$2.99

$0

The advantage of amortization is that you can slowly pay back the interest on the loan, rather than paying one huge balloon payment at the end. The downside of spreading the payments over 30 years is that you end up paying $215,838 for that original $100,000 loan.

The total cost of a mortgage loan depends on the interest rate, as well as the length of the mortgage. The longer you finance for, the more you’ll pay if all other factors are the same. Consider the examples below.

$100,000 mortgage at 3.92 interest for 30 years equals a total cost of $170,213 and a monthly payment of $473

$100,000 mortgage at 3.92 interest for 15 years equals a total cost of $132,423 and a monthly payment of $736

If you have questions about mortgage interest rates or payments, don’t hesitate to reach out! We are experts at guiding buyers through the home buying process and are here to help in any way we can.

This blog post was written by experts at Mortgage 1 and originally appeared on www.mortgageone.com. Michigan Mortgage is a DBA of Mortgage 1.

https://www.michmortgage.com/wp-content/uploads/2020/09/Charts.jpg620620mimortgagehttp://www.michmortgage.com/wp-content/uploads/2017/12/MM-for-white-background-300x105.pngmimortgage2020-09-24 11:08:442020-09-24 11:15:50Calculating Mortgage Interest Rates and Payments

The Doctor Loan has a long history in the United States. First offered to attract new physicians to growing towns in the Wild West, they have evolved over the year. Today, 18,000 new physicians graduate from medical school every year. New physicians can have very specific credit and income profiles that represent a different kind of risk, not reflected in a normal borrower profile.

What Is a Physician Mortgage Loan?

A physician mortgage loan is a low down payment mortgage available to physicians, dentists and other eligible medical professionals. They do not require mortgage insurance and are often considered jumbo mortgages as they allow higher loan balances than conventional and FHA mortgage loans. These doctor home loans have fewer restrictions for borrowers than conventional loans because lenders generally trust doctors to be responsible borrowers.

At Michigan Mortgage, we’ve made it easy for doctors to get a physician mortgage.

The Michigan Mortgage Physician Mortgage Loan Program

That is why Michigan Mortgage has a very specific program designed for that type of individual. Physicians of all types can benefit from our “Doctor Loans.” Features of the program include:

Available for new residents, new attending (7-10 years out of residency), or to physicians at any stage of their career.

Flexible down payment options.

Private mortgage insurance (PMI) is not required.

Rather than looking for past income, we will consider an employment contract as documentation of future earnings (instead of pay stubs.

The loan amount can go all the way up to $2 Million.

Can be used for primary or second home.

Certain programs allow new Physicians to use gift money for a down payment, for required reserves, or for closing costs.

Often doesn’t calculate student loans the same way as standard underwriting. Student loans are not counted as part of debt-to-income ratio (DTI).

Other than a doctor loan, physicians are also available for other loan types.

Conventional Mortgage: Often this is the best choice for borrowers. Conventional loans generally offer the most term options and lowest fees, with the lowest rates. Conventional loans do require proof of earnings and a substantial sum of money (20% of mortgage amount) to put down.

FHA Loan: This loan can have higher fees and rates than a conventional mortgage. FHA mortgages can have a smaller required down payment, and a monthly mortgage insurance premium. This loan requires the lender to use the credit report amount of the student loan payment, or if none listed, 1 percent of the outstanding balance unless the borrower can provide documentation that the loan is in deferral. The interest rate could be slightly lower than a Doctor Loan but could wind up costing more because of PMI costs.

VA Loan: This loan requires that you qualify for VA benefits. There is no down payment or mortgage insurance requirement. Rates are similar to FHA rates, but the funding fee is slightly higher.

Ready to get started with a Doctor Loan? Give us a call and we will guide you through the process!

This blog post was written by experts at Mortgage 1 and originally appeared on www.mortgageone.com. Michigan Mortgage is a DBA of Mortgage 1.

https://www.michmortgage.com/wp-content/uploads/2020/07/House-for-sale.jpg620620mimortgagehttp://www.michmortgage.com/wp-content/uploads/2017/12/MM-for-white-background-300x105.pngmimortgage2020-07-09 09:22:202020-08-19 21:19:38Doctor Loans: What You Need to Know

Your three-digit credit score can make or break your financial future.

Interested in buying a home? Your credit score will determine whether or not you qualify. Looking to buy a new car or recreational vehicle? Your credit score will determine your interest rate. Hoping to take out a personal loan to invest in your child’s future? You need to have good credit to do so.

If your credit score isn’t up to par, we’re here to help! But before we offer you tips to improve your three-digit score, we want to make sure you understand how your score is calculated.

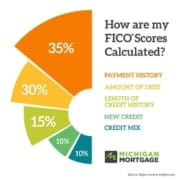

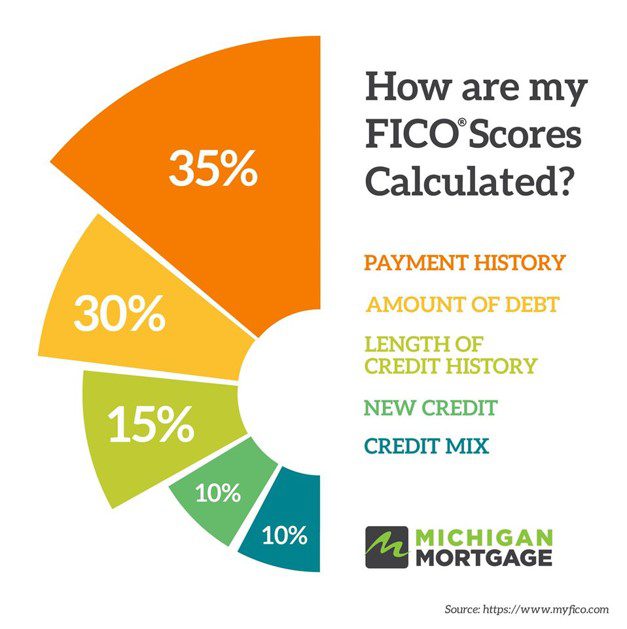

A combination of five factors determines your FICO credit score; some factors impact the score more than others. Take a look at the graph below to better understand.

FICO scores can range from 300 to 850, but for mortgage purposes, your goal should be 680 or above.

Here are five tips to help you reach that 680 benchmark.

Make sure your credit reports are accurate. Lenders analyze reports from three credit bureaus when you apply for a mortgage – Equifax, TransUnion and Experian. If you don’t have a copy of your reports, you can claim a free report from each bureau once every 12 months at annualcreditreport.com. Mistakes are known to happen, and reporting errors can have a negative impact on your score. If you find a credit reporting error, dispute the mistakes with the appropriate credit reporting agency and your score may improve.

Make your payments on time. According to experts, a large portion of your credit score (35 percent, to be exact) is calculated based on payment history. Making your payments on time, every time can greatly impact your score. This includes credit card bills or any loans you may have, such as auto loans or student loans, your rent, utilities, phone bill and so on.

Reduce the amount you owe. Roughly 30 percent of your credit score is calculated based on the amount of debt you owe. Most loan programs have very specific debt-to-income ratios in place that can keep you from purchasing your dream home. For the ultimate credit score boost, credit experts suggest you pay on time, twice per month, and decrease the amount you owe. This will help control the factors that collectively make up 65 percent of your score.

Become an authorized user on someone else’s credit card account. This is easier said than done, but if your spouse or parent has excellent credit and a perfect payment history, it would benefit you (and improve your credit score) if you were added as an authorized user on their credit card account. Why? The account will show up on your credit report as well as the credit utilization rate and all the on-time payments associated with the account, which will naturally increase your score.

Open a secure credit card. Opening a secure credit card, and using it properly, can help to increase your credit score. You’ll be required to deposit money into a checking account to secure the line of credit. Payments will come directly out of this account, so they will always be on time and will never be missed.

Your credit score won’t improve over night, but with a little hard work and dedication, you’ll be moving into your dream home in no time.

https://www.michmortgage.com/wp-content/uploads/2020/04/FICO-Score.jpg629627Courtney Coonhttp://www.michmortgage.com/wp-content/uploads/2017/12/MM-for-white-background-300x105.pngCourtney Coon2020-04-02 09:04:492020-04-02 09:06:06Five Tips to Improve Your Credit Score

These are certainly crazy times. The COVID-19 Pandemic has the markets in turmoil. Many states, including Michigan, have issued stay home orders, and people are generally anxious about the future. People are looking for options and smart decisions.

One of the options many people have so that they feel more secure, is to do a cash-out refinance on their home. Let’s take a closer look at some of the benefits and possible downfalls of this.

There are three reasons that I generally advise as sound financial reasons to do a cash-out refinance:

Home Repairs

Pay Off Debt

Conservative Investments with a Financial Advisor

We will Address Each of these reasons in more detail below, but before we can get to the reasons, it is important to determine whether there is enough equity in your home to pull cash out. Equity is the difference between what you owe and what your house is worth. Generally, banks will not allow more than 80 percent of the appraised value to be pulled out in a cash-out refinance. Your lender will most likely need to do an appraisal to determine value; however, you can utilize sites like Zestimate to get a general idea.

Home Repairs

Pulling out equity to do home repairs not only adds value to your life, it oftentimes adds value to your home. If the added value is more than the cost to do the work, you have just made a good investment. So even though you added closing costs and principle to your loan, you could be ahead of the game when you do end up selling.

Paying Off Debt (Debt Consolidation)

Paying off credit card debt and high interest debt is usually met with enthusiasm from the client. This debt is oftentimes weighing heavily on client’s monthly expenditures and is gladly paid off. We will address precautions regarding that below.

Other than paying off credit cards, there are options to pay off other debt. Oftentimes clients balk at adding debt to their mortgage to pay off shorter term installment debt. The argument is that paying off this is unwise because it is added to a longer term on a mortgage. I hear things like “I only owe five years on the car, so I don’t want to add that to a 15-year mortgage.” The problem with this argument is that they are not thinking about what could be done with the money they are freeing up.

Here is the math:

Lets’ say someone has a $20,000 installment loan at 6% interest paying $386/mo. After 5 years they will have paid $23,160. If they were to consolidate that into a 15-year mortgage at 3% they would pay $24,840 in 15 years. But that is $1, 600 more you say? True BUT what if you took that $386 that you freed up and invested conservatively? Making just 5% compounded annually over the 5 years you would make $25,594! If you kept that up for 15 years you would make $99,951!

Investments

Pulling out equity to make investments is a bit trickier. I do not normally advise this unless it is part of a financial plan overseen by a trusted financial advisor. The argument for investing is similar to the one that I made above. The problem is that investing is not for the weak of heart and hopeful gains can sometimes become devastating losses. If someone is going to pull out equity in their homes to invest, they need to have a CONSERVATIVE plan that has a high likelihood of success. Again, you really should have a financial advisor in on this plan.

Side Benefits of Doing a Cash-Out Refinance

Aside from home improvement, paying off debt and investing, a cash-out refinance might afford you the ability to lower your interest rate or remove mortgage insurance. This is especially true in the current market where interest rates have fallen and values of homes have risen.

Pitfalls to a Cash-Out Refinance

Possible higher rate. As compared to a rate and term refinance (not pulling out extra equity), the interest rates on a cash out can be higher depending on your equity position.

Enabling bad habits. Using them money to pay for vacations or buy non-essential luxury items is not a good idea for obvious reasons. Paying off credit cards can be a great idea as mentioned above, but if you then run up the cards again in a few months you have defeated the purpose. Be smart and don’t succumb to the allure of credit card debt.

Foreclosure risk. Remember that a mortgage is a secured debt. If you don’t pay you can lose your home. Paying off unsecured debt with secured debt can be a risk if you simply cannot afford your debt. Occasionally, I have clients that come to my trying to solve all of their previous bad decisions with a cash-out refinance. Sometimes I can help but oftentimes, doing this is just prolonging the inevitable: they simply have too much debt and not enough equity to save the day.

Bottom Line

Using a cash-out refinance can make sense when interest rates are good and you have a sound use for the money. Do not use it as a rescue maneuver that could cause you to lose your home or to buy something you don’t need. In these trying times, it is imperative that you have good advice. We can guide you and help you make the best decision for your unique situation.

https://www.michmortgage.com/wp-content/uploads/2018/06/Mortgage-Interest-Rates.jpg620620Rob Garrisonhttp://www.michmortgage.com/wp-content/uploads/2017/12/MM-for-white-background-300x105.pngRob Garrison2020-03-22 07:55:212020-04-08 11:13:34The Pros and Cons of a Cash-Out Refinance

Your debt-to-income (DTI) ratio is the percentage of your income that goes toward paying your monthly debts. DTI can often be overlooked as many people assume that a good credit score and a high income are the only two factors needed to be taken into consideration when seeking to purchase a home.

However, for many lenders, that’s not enough to be considered a good mortgage candidate. As a borrower, your DTI is utilized in various situations to determine your level of risk. For instance, if your DTI is too high, opportunities to make a big purchase, such as a mortgage, may be limited.

How to Calculate Your DTI Ratio

DTI Ratio = (Monthly expenses ÷ Pre-Tax Income) x 100

Start by adding up your monthly bills such as:

Rent or house payment

Alimony or child support

Student loans

Auto payments

Other

Next, divide your total sum by your gross monthly income (income before taxes). Multiply by 100. Your result is your DTI ratio.

The goal is to keep your DTI ratio as low as possible. The lower the ratio, the less risky you are to lenders. An adequate DTI ratio is below 36 percent. Typically, having a DTI ratio of 43 percent is the maximum ratio you can have in order to be qualified for a mortgage.

Front-End DTI vs. Back-End DTI

There are two variations of DTI: Front-End and Back-End.

A front-end DTI calculates how much of a person’s gross income is going towards housing costs. Front-End DTI = (Housing Expenses ÷ Gross Monthly Income) x 100

A back-end DTI calculates the percentage of gross income going toward other types of debt (credit cards, car loans, etc.). Back-End DTI = (Total monthly debt expense ÷ Gross Monthly Income) x 100

The main difference between Front-End and Back-End DTI ratios is that the front-end ratio only considers the mortgage payment and other housing expenses whereas the back-end ratio considers all other types of debt. Lenders will utilize this ratio in conjunction with the front-end ratio to approve mortgages.

Why is Knowing Your DTI Ratio Important?

Your DTI ratio is utilized by lenders as a measuring tool. Your DTI ratio helps lenders determine your ability to manage your finances, specifically, your monthly payments to repay the money you borrowed. Keep in mind that lenders do not know what you will do with your money in the future, so they refer to historical data to verify your income and debt totals. Moreover, your DTI ratio illustrates that you have a sufficient balance between your income and debt, thus, are more likely to be able to manage your mortgage payments.

If you are considering buying a home or have questions about your DTI ratio, give us a call!

This blog post was written by experts at Mortgage 1 and originally appeared on www.mortgageone.com. Michigan Mortgage is a DBA of Mortgage 1.

https://www.michmortgage.com/wp-content/uploads/2019/08/Building-blocks.jpg360360Rob Garrisonhttp://www.michmortgage.com/wp-content/uploads/2017/12/MM-for-white-background-300x105.pngRob Garrison2019-10-24 09:34:332020-01-16 16:33:03What is debt-to-income ratio?

A house is the biggest purchase most people make in their lifetimes. The mortgage they obtain to finance that house is likely the biggest single investment they will ever make.

Even with the popularity of shorter terms and creative loans, most mortgages are still the tried-and-true 30-year conventional variety. First-time home buyers staring down the gauntlet of 360 payments spread over the next three decades of their life can feel like there is no end in sight. And for those who dare to look at their amortization schedules, that no-end-in-sight feeling can be even greater.

But there is a way to get ahead of the game: making extra mortgage payments.

Why It Makes Sense to Make Extra Mortgage Payments

Why does it make sense to make extra mortgage payments? Put simply, you will save significant amounts in interest. Most mortgage contracts allow borrowers to make extra payments, and they allow all of the extra money to be applied to the principal amount of your loan. That means you are paying down the real amount of the loan – the money you borrowed – faster. Because the interest part of your loan is calculated on the amount of principal you still owe, reducing your principal amount greatly reduces the interest amount.

According to the web site interest.com, “a $200,000 30-year home loan with an interest rate of 5% would cost $186,512 in interest with the traditional 12 payments a year. Make the equivalent of 13 monthly payments every year, and the loan will be retired in 26 years and you will pay only $153,813 in interest — a savings of $32,699.”

That’s nothing to sneeze at.

How to Make Extra Mortgage Payments

When it comes to making extra payments on your mortgage, there are a variety of tactics that can be used. Each has the same goal in mind: to reduce the principal and, thereby, reduce interest.

The tactics for making extra mortgage payments include the following.

Accelerated Payment Schedule

Rather than making your mortgage payment once per month, or the equivalent of every four weeks, you could make payments every two weeks. This biweekly payment plan results in 26 half-payments, which is the equivalent of 13 full payments for the year. The extra payment each year can shave off eight years from a 30-year loan.

Extra Principal with Each Monthly Payment

If you’re looking to chip away at your mortgage at a more gradual pace, pay a little extra each month. Check with your lender to make sure the additional payment goes directly to the principal. Depending on how much extra principal you pay, you could shorten your loan significantly. And, best of all, because your are shortening the loan duration, you will save significant amounts in interest.

One Additional Payment Per Year

Another tactic is to make one additional, principal-only payment per year. Some people who do this use their income tax refund for this purpose.

One Additional Payment Per Quarter

Making an additional payment each quarter results in four extra payments per year. On a $220,000, 30-year mortgage with a 4% interest rate, you would cut 11 years off your mortgage and save $65,000 in interest.

Lump-Sum Payment

Applying a lump-sum payment toward your principal balance when you come into extra cash — a bonus at work, a sizable inheritance — can shave time from your mortgage. This approach isn’t as consistent as some of the other methods, but, if the lump payment is large enough and depending on where you are in your timeline, it can eliminate many years.

This blog post was written by experts at Mortgage 1. Michigan Mortgage is a DBA of Mortgage 1.

https://www.michmortgage.com/wp-content/uploads/2019/07/Large-home-and-yard.jpg288288Courtney Coonhttp://www.michmortgage.com/wp-content/uploads/2017/12/MM-for-white-background-300x105.pngCourtney Coon2019-07-25 13:15:072019-07-25 13:15:07Advantages of Making Extra Mortgage Payments

A mortgage is a loan, and like other bank loans, it comes with an interest rate – it’s how lenders make enough money to stay in business. This is usually a percentage of the loan amount, and you pay it off alongside the principal. Usually, this makes up your monthly mortgage payment, along with things like private mortgage insurance (PMI), property taxes, and perhaps homeowner insurance.

A mortgage is a loan, and like other bank loans, it comes with an interest rate – it’s how lenders make enough money to stay in business. This is usually a percentage of the loan amount, and you pay it off alongside the principal. Usually, this makes up your monthly mortgage payment, along with things like private mortgage insurance (PMI), property taxes, and perhaps homeowner insurance.

Let’s assume a home is being sold for $300,000 and the buyer is putting 5% down. To attract more buyers, the seller has agreed to pay $6,100 toward a 2-1 Buydown. If the current market rate is 5.5% then the buyer’s payment for the first 12 months would be at 3.5% or $1,279/month. For the second year, the payment would be based on a rate of 4.5% or $1,444/month. Starting in the third year, the buyer’s payment would be at 5.5% for the remaining 28 years or $1,618/month.

Let’s assume a home is being sold for $300,000 and the buyer is putting 5% down. To attract more buyers, the seller has agreed to pay $6,100 toward a 2-1 Buydown. If the current market rate is 5.5% then the buyer’s payment for the first 12 months would be at 3.5% or $1,279/month. For the second year, the payment would be based on a rate of 4.5% or $1,444/month. Starting in the third year, the buyer’s payment would be at 5.5% for the remaining 28 years or $1,618/month.

For first-time buyers, the mortgage process raises a lot of questions. In part two of this series, we tackle some more of the most common questions we receive from customers.

For first-time buyers, the mortgage process raises a lot of questions. In part two of this series, we tackle some more of the most common questions we receive from customers.

Technically speaking, “A mortgage is a debt instrument secured by the collateral of specified real estate property, that the borrower is obliged to pay back with a predetermined set of payments.” (Investopedia.com)

Technically speaking, “A mortgage is a debt instrument secured by the collateral of specified real estate property, that the borrower is obliged to pay back with a predetermined set of payments.” (Investopedia.com)

Interest is what makes all forms of borrowing possible. Interest is the fee a lender charges for loaning money.

Interest is what makes all forms of borrowing possible. Interest is the fee a lender charges for loaning money.

What Is a Physician Mortgage Loan?

What Is a Physician Mortgage Loan?

However, for many lenders, that’s not enough to be considered a good mortgage candidate. As a borrower, your DTI is utilized in various situations to determine your level of risk. For instance, if your DTI is too high, opportunities to make a big purchase, such as a mortgage, may be limited.

However, for many lenders, that’s not enough to be considered a good mortgage candidate. As a borrower, your DTI is utilized in various situations to determine your level of risk. For instance, if your DTI is too high, opportunities to make a big purchase, such as a mortgage, may be limited.

Even with the popularity of shorter terms and creative loans, most mortgages are still the tried-and-true 30-year conventional variety. First-time home buyers staring down the gauntlet of 360 payments spread over the next three decades of their life can feel like there is no end in sight. And for those who dare to look at their amortization schedules, that no-end-in-sight feeling can be even greater.

Even with the popularity of shorter terms and creative loans, most mortgages are still the tried-and-true 30-year conventional variety. First-time home buyers staring down the gauntlet of 360 payments spread over the next three decades of their life can feel like there is no end in sight. And for those who dare to look at their amortization schedules, that no-end-in-sight feeling can be even greater.