How Your Credit Score Impacts the Home-Buying Process

Your credit score plays a crucial role in the home-buying journey. Whether you’re just beginning to think about purchasing a home or already shopping for mortgage options, understanding how your credit impacts the process can help you plan ahead and secure the best possible deal.

Why Credit Scores Matter

Mortgage lenders use your credit score to evaluate how likely you are to repay your loan. The higher your score, the more favorable your terms will likely be. Here’s how your credit score can affect the process.

-

Loan Approval: Most lenders require a minimum credit score to qualify for a mortgage. Conventional loans often require at least a 620, while FHA loans may accept scores as low as 580.

-

Interest Rates: A higher credit score usually results in a lower interest rate, which can save you thousands over the life of your loan.

-

Loan Programs: Some government-backed loans or first-time homebuyer programs may only be available to borrowers with certain credit thresholds.

-

Private Mortgage Insurance (PMI): If your credit score is lower, you may pay higher PMI premiums if you put down less than 20%.

Tips to Improve Your Credit Score

Improving your credit score can take time, but small, consistent steps can make a big difference.

-

Check Your Credit Reports: Review your reports from all three major bureaus (Experian, Equifax, and TransUnion) to ensure there are no errors or outdated information.

-

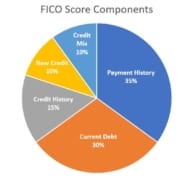

Pay Bills on Time: Payment history makes up a large portion of your score. Set reminders or automate payments to avoid late fees.

-

Reduce Credit Card Balances: Keep your credit utilization below 30% of your available limit. Paying down high balances can quickly boost your score.

-

Avoid Opening New Accounts: Each new account triggers a credit inquiry, which can slightly lower your score. Hold off on opening new credit lines during the mortgage process.

-

Keep Old Accounts Open: The length of your credit history affects your score. Don’t close old cards, even if you don’t use them often.

Final Thought

Your credit score can open doors — or create obstacles — in the home-buying process. By taking control of your credit now, you’ll be in a stronger position when you’re ready to make an offer on your dream home.

Need help understanding how your credit score affects your mortgage options? Reach out — we’re here to guide you every step of the way!