First-Time Buyer FAQ

For first-time buyers, the mortgage process raises a lot of questions. In this article, we tackle some of the most common questions we receive from customers.

“How Does a Mortgage Work?”

Technically speaking, “A mortgage is a debt instrument secured by the collateral of specified real estate property, that the borrower is obliged to pay back with a predetermined set of payments.” (Investopedia.com)

Technically speaking, “A mortgage is a debt instrument secured by the collateral of specified real estate property, that the borrower is obliged to pay back with a predetermined set of payments.” (Investopedia.com)

What does that mean in plain English? It means, when you get a mortgage, you are (1) borrowing money from a lender and (2) committing yourself to paying back the money you borrowed in equal monthly payments for the length of the loan.

Because a house can be expensive, mortgage payments are usually spread over 15 or 30 years, making the cost affordable.

Your mortgage payment will consist of principal and interest portions. The principal portion goes toward reducing the amount of money you originally borrowed. The interest portion goes toward paying off the interest, which you can think of as the fee the lender charges to loan you money.

You can make additional payments, if you want, but at the least you need to make your minimum monthly payment each month.

“What Types of Loans Are There?”

Mortgage lenders offer a wide variety of loans designed to meet the needs of buyers. The most common types of loans obtained by first-time buyers are:

- Conventional loans. This is the most common type of mortgage loan. Conventional loans can be for as long as 30 years or as short as five years, with options in between. They can be fixed-rate or adjustable rate. Conventional loans are provided by banks as well as private mortgage lenders like Mortgage 1. When most people think about home loans, the conventional loan is the one they are thinking of.

- FHA loans. A Federal Housing Administration (FHA) loan is a mortgage that is insured by the Federal Housing Administration (FHA) and issued by an FHA-approved lender such as Mortgage 1. FHA loans are designed for low-to-moderate-income borrowers; they require a lower minimum down payment and lower credit scores than many conventional loans.

- VA loans. VA loans are offered through the Department of Veterans Affairs. They are available to active and veteran service personnel and their families. VA loans are backed by the federal government and issued through private lenders like Mortgage 1. VA loans have favorable terms, such as no down payment, no mortgage insurance, no prepayment penalties and limited closing costs.

- USDA loans. Rural Development home loans are low-interest, fixed-rate loans provided by the United State Department of Agriculture. The loans do not require a down payment. The loans are financed by the USDA and obtained through private lenders, such as Mortgage 1, and are meant to promote and support home ownership in underserved areas.

- MSHDA loans. The Michigan State Housing Development Authority (MSHDA) offers down payment assistance to people with no monthly payments. The down payment program offers assistance up to $7,500 (or 4% of the purchase price, whichever is less).

“How Do I Qualify for a Mortgage?”

Different mortgage types have different specific qualification requirements, but the general process of qualifying for a mortgage is the same.

- You submit an application with a lender.

- You provide the necessary documentation, which includes paycheck stubs, tax statements, bank and asset statements, and identification.

- The lender reviews your information. They look at your income, how much debt you have, and they also pull a credit report.

- Based upon your status, the lender determines how much money you can afford for a mortgage as well as what interest rate you should receive.

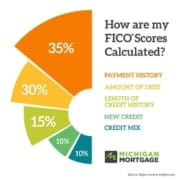

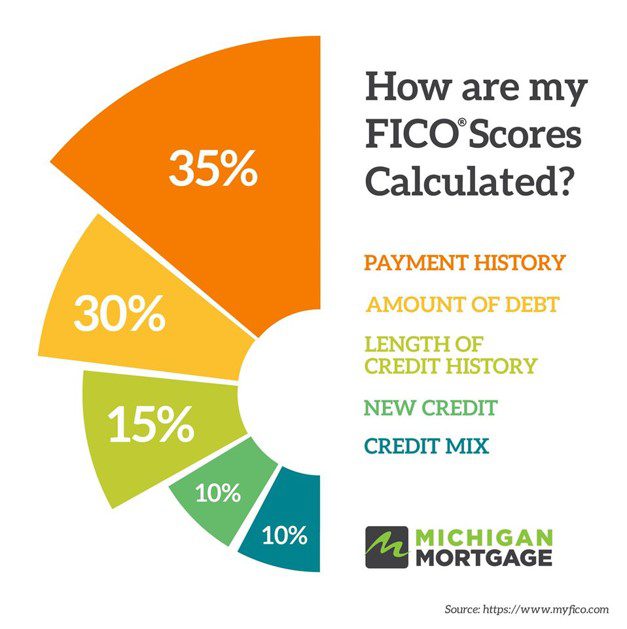

“What Is the Required Minimum Credit Score?”

An important element of qualifying for a mortgage is your credit score. Your lender pulls a credit report to look at your credit score. Different loan types have different qualifying scores:

- The minimum qualification score for most conventional loans is 620.

- For FHA loans, the minimum score is 580.

- For VA loans, the minimum score is 620.

- For USDA loans, the minimum score is 640.

In addition to credit score, a lender looks at your debt-to-income ratio to make sure you are not overextended.

“How Much House Can I Afford?”

To determine how much house you can afford, follow the 28/36 rule.

Many financial advisers agree that households should spend no more than 28 percent of their gross combined monthly income on housing expenses and no more than 36 percent on total debt. Total debt includes housing as well as things like student loans, car expenses, and credit card payments.

The 28/36 percent rule is the tried-and-true home affordability rule that establishes a baseline for what you can afford to pay each month.

To calculate how much 28 percent of your income is:

- Multiply 28 by your monthly income. If your monthly income is $7,000, then multiply that by 28. 7,000 x 28 = 196,000.

- Divide that total by 100. For example, 196,000 ÷ 100 = 1,960.

Do the same for the 36 percent rule, using 36 in place of 28 in the example above.

Got Questions? We’ve Got Answers

Come back next week for part two of this article. In the meantime, if you have questions, let us know. At Michigan Mortgage, we specialize in helping first-time buyers understand the mortgage process.

This blog post was written by experts at Mortgage 1 and originally appeared on www.mortgageone.com. Michigan Mortgage is a DBA of Mortgage 1.

Interest is what makes all forms of borrowing possible. Interest is the fee a lender charges for loaning money.

Interest is what makes all forms of borrowing possible. Interest is the fee a lender charges for loaning money.

The Benefits of Owning a Vacation Home

The Benefits of Owning a Vacation Home

Step 1: Check Your Credit Score

Step 1: Check Your Credit Score

1. Personalized Service

1. Personalized Service

What Is a Physician Mortgage Loan?

What Is a Physician Mortgage Loan?

What Are the Benefits of a USDA Loan?

What Are the Benefits of a USDA Loan?

Conventional Loan

Conventional Loan

It is important for you to analyze your spending habits. If you do not have a budget, you should start one now. This will help you understand you spending habits so that the lifestyle that is important to you will be maintainable as a homeowner.

It is important for you to analyze your spending habits. If you do not have a budget, you should start one now. This will help you understand you spending habits so that the lifestyle that is important to you will be maintainable as a homeowner.